Discover financial empowerment resources

Discover financial empowerment resources

When Canadians have a financial problem, want to make a financial plan, or need help with their taxes, most simply reach out to their financial institution, adviser, accountant, or commercial tax preparer for the help they need. But who do low-income individuals turn to? A new report by Prosper...

A new study by national charity Prosper Canada, undertaken with funding support from Co-operators, finds that Canadians with low incomes are increasingly financially vulnerable but lack access to the financial help they need to rebuild their financial health. The report, shows that affordable,...

Canada’s external complaint handing structures and processes play a critical role in levelling the playing field for consumers and financial service providers, helping to offset the inevitable imbalance of power between large financial institutions and individual consumers. Prosper Canada...

Almost half of low-income households and 62 per cent of moderate-income households carry debt, with households on low incomes spending 31 per cent of their income on debt repayments, according to a new report published by national charity, Prosper Canada. This report analyzes the distribution,...

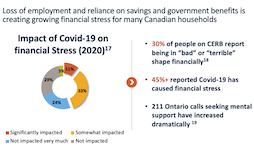

Even before the COVID-19 pandemic, many Canadians were having difficulty making ends meet, and the pandemic has further impacted the financial well-being of financially vulnerable Canadians. In this webinar, we present research on how COVID-19 has impacted the financial security of Canadians and...

Prosper Canada and AFOA Canada are pleased to collaboratively tell the story of The Shared Path: First Nations Financial Wellness. This work was undertaken in the spirit of reconciliation between Indigenous Peoples and non-Indigenous people in Canada and creating a more equitable and inclusive...

This article in the Economic Insights series from Statistics Canada examines the economic well-being of millennials by comparing their household balance sheets to those of previous generations of young Canadians. Measured at the same point in their life course, millennials were relatively better...

Income volatility is increasing in the United States and presents a growing public health problem. This study examines associations of long-term income volatility with incident cardiovascular disease and all-cause...

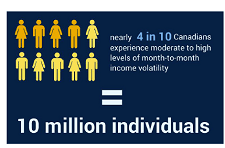

A growing number of Canadians are living with fluctuating incomes - incomes which may vary significantly from month to month, not just from year to year. This makes it difficult to save, plan, and achieve financial wellness. This webinar, "Income volatility in Canada: Why it matters and what to do...

This webinar, "Indigenous financial wellness in Canada," introduces an Indigenous financial wellness framework, identifies some of the key barriers and opportunities for building financial wellness in Indigenous communities, and highlights evidence-based best practices for building financial...

There was a time, not very long ago, when Canadians were savers. In 1982, we routinely set aside 20 percent of our yearly income for large household purchases, education, starting businesses, retirement or just plain rainy days. Having a savings ‘nest egg’ was accepted wisdom and the norm. Then...

Financial education plays an important role in guiding individuals to achieve their financial goals and contribute to the economic well-being of society as a whole. While the examination on the effectiveness of financial education has many factors to consider, the National Endowment for Financial...

This introductory article by guest editor, Elizabeth McIsaac of Maytree, provides an overview of the strategies and policies for rights-based poverty reduction in Canada beginning with the need for common language and goals. Referring to the International Covenant on Economic, Social and Cultural...

This scan of financial counselling best practices was undertaken in response to a growing demand among low-income consumers in Canada for personalized financial support to help them tackle complex financial issues, gain access to income boosting entitlements, and plan for their financial futures....

Indicators are the data that help you assess whether or not you are on track to achieve the desired results identified in your logic model. They are also useful to communicate your program’s potential impact to funders and stakeholders. Programs that consistently collect and review data to track...

An important part of program design is determining how to assess the program’s effects on the clients and their community. Typically, we assess program effectiveness by measuring the changes in outcomes—the changes in the conditions of your clients, their families and their communities—that...

A well-designed logic model can provide the foundation to support your efforts to collect the data necessary to answer important questions about the performance of the program. A logic model can be developed and formatted in many ways. In this document, we are not prescribing the “best...

Using information from the FINRA Investor Education Foundation 2012 National Financial Capability Study, we examined financial capability among people with and without disabilities. Respondents noted as having disabilities throughout this report selected “permanently sick, disabled, or unable to...

This is the video recording of the AFOA 2014 Conference panel on Indigenous Financial Literacy. In this session, Liz Mulholland, Dr. Paulette Tremblay, Simon Brascoupe, and Darren Googoo discuss Indigneous financial wellness, financial literacy, and community...

The Canada Learning Bond (CLB) is an educational savings incentive that provides children from low income families born in 2004 or later with financial support for post-secondary education. Personal contributions are not required to receive the CLB, however take-up remains low among the eligible...