Discover financial empowerment resources

Discover financial empowerment resources

Food insecurity is a significant public health problem for Indigenous peoples in Canada. A comprehensive literature review is needed to organize the evidence according to the 4 pillars of food security (i.e., availability, access, utilization, and stability) and identify gaps in the published...

Robo-advisors first arrived in Canada in the beginning of 2014 presenting young and middle-income investors the option of having their savings passively managed in a bundle of exchange-traded funds (ETFs) matched to their goals and risk tolerance for about a penny on the dollar per year: A perfect...

COVID-19’s effects have underscored the ways that racism, bias, and discrimination are embedded in health, social, and economic systems. Black, Indigenous, and Latinx people are experiencing higher rates of infection, hospitalization, and death, and people of color are also overrepresented in...

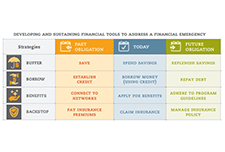

Financial shocks like these happen to financially vulnerable families every day. Such shocks destabilize household finances and can create hardships that threaten overall well-being. Having tools to manage financial emergencies is critical for people’s long-run financial security. The Asset...

The Asset Funders Network (AFN) developed this primer to inform community-based strategies that can help economically-vulnerable families to better manage financial setbacks, shortfalls, and shocks. The goal of this brief is to provide a common understanding and language for funders and financial...

Financial stress is the root cause of many adverse health outcomes among poor and low-income children and their families, yet few clinical interventions have been developed to improve health by directly addressing patient and family finances. Medical-Financial Partnerships (MFPs) are novel...

Modern financial planning is dominated by one topic: retirement planning. However, in spite of extensive study and wide attention, retirement savings rates remain perplexingly low and remarkably resistant to policy intervention. One approach that does seem to work is employer-based education....

This is an editorial opinion written by J. Michael McGinnis, MD, MPP, on findings by John Hopkins Boomberg School of Public Health connecting life expectancy with income level. It has long been known from national-level data that incomes and standards of living are associated with life expectancy,...

BDSC firms are using varied forms of non-traditional data—from mobile call data records and bill payments to Internet browsing patterns and social media behaviour—to create a new way to assess consumer risk, determine the creditworthiness of previously “invisible” consumers, and...

This is a presentation by J. Michael Collins explaining why financial coaching is a more effective intervention to achieve financial capability, compared to financial literacy. He explains the role of counseling, a definition of financial coaching, the role of the coach, and coaching as a form of...

This article explores benefits screening, a system of auditing patients to identify those living in poverty and the benefits they may be eligible for, as an innovative step towards realizing the right to health in Canada by advancing health equity. In particular, it assesses one online tool...

This presentation examines the financial coaching model and suggests an approach to measure outcomes of financial coaching and financial...

Canadians with disabilities have consistently experienced low levels of employment, as well as barriers in the educational, economic and social spheres. They face massive obstacles in participating in the labour market, especially those with severe disabilities or low educational attainment....

This pilot study explores the delivery and effectiveness of MyBudgetCoach, a financial coaching program designed to help low- and moderate-income adults develop budgeting skills, set financial goals, and work towards those goals. Specifically, this study compares two modes of program delivery,...

Almost all poverty measures commonly used in Canada work by setting a dollar amount – a poverty line – below which a household is said to be in poverty, above which a household is not considered poor. But when we measure poverty only according to income, we may incorrectly assess whether or not...

This pilot study explores the delivery and effectiveness of MyBudgetCoach, a financial coaching program designed to help low- and moderate-income adults develop budgeting skills, set financial goals, and work towards those goals. Specifically, this study compares two modes of program delivery,...

This brief summarizes key findings from a pilot study of MyBudgetCoach (MyBC).1 MyBC is a financial coaching program designed to help low- and moderate-income adults develop budgeting skills and work towards their financial goals. Trained coaches use the program’s online platform...

Financial coaching is a promising strategy to help people improve their financial well-being, but is often not yet universally understood. Practitioners are turning to coaching strategies to better facilitate behaviour change as opposed to the disappointing results often found when only financial...

According to a 2013 Federal Reserve Board Survey, technology is increasingly being used by people at all income levels to manage basic financial tasks. With the popularity of smart phones increasing the convenience and accessibility of the internet, combined with the ever increasing public access...

Using information from the FINRA Investor Education Foundation 2012 National Financial Capability Study, we examined financial capability among people with and without disabilities. Respondents noted as having disabilities throughout this report selected “permanently sick, disabled, or unable to...

Population health survey data are not routinely linked to specific health care organizations, limiting organizational capacity to assess performance improvements in relation to the observed risk and prevalence of differences in health. The lack of demographic information hinders the growth of...

The Center for Financial Security (CFS) and Annie E. Casey Foundation have developed a short set of standardized client outcome measures to create the Financial Capability Scale (FCS). In 2011, CFS worked with four organizations to collect data on client outcome measures, with the goal of...

In the spring of 2012, the Center for Financial Security (CFS) interviewed financial coaches at 11 organizations in order to document emerging practices and ongoing challenges for the field. The organizations were selected based on prior familiarity and through suggestions from CFS coaching...

Financial counselling may be an effective way to improve individuals’ financial behaviour and outcomes. However, its impacts have not been adequately studied. Previous studies show weak positive effects of counselling, but are subject to a number of limitations. This study, a collaboration...

Financial literacy has been proposed widely as an effective approach to preparing people to manage their finances. This paper proposes an alternative concept, financial capability. Financial capability includes both the ability to act (knowledge, skills, confidence, and motivation) and the...