Discover financial empowerment resources

Discover financial empowerment resources

The National Financial Empowerment Champions (NFEC) Project supported leading non-profit community organizations and their local partners to develop, implement and scale proven financial empowerment (FE) interventions across Canada with the aim of improving the financial well-being of over one...

In this moment, it is pivotal for philanthropy to support communities of color in achieving financial well-being. Combined with systems-change efforts that would create fairer economic opportunities and conditions, financial coaching is a vital component of providing needed support. Through...

Practitioners engaged in the nascent field of financial development lack a shared system of tracking and analyzing customer progress toward financial security. Practice leaders—ranging from direct service organizations such as the Chicago-based LISC to NeighborWorks America of Washington,...

This report was originally developed to support the work of Feeding America and its member food banks in exploring interventions that support households’ economic well-being. Such strategies can be valuable not only for organizations serving households facing food insecurity, but for agencies and...

This resource offers a set of common indicators that community organizations can use to measure the reach and impact of their financial empowerment (FE) programming. It is intended for any community organization that works to foster greater financial well-being for economically disadvantaged...

Despite the well-documented connection between health and wealth, investing in this intersection is still a new approach for many grantmakers. With the goal of inspiring increased philanthropic attention, exploration, and replication, this new spotlight elevates responsive philanthropic strategies...

The Local Initiative Support Corporation (LISC) developed the strategy Building Sustainable Communities to tackle pressing need through an expansive network of Financial Opportunity Centers (FOCs) in dozens of communities nationwide. FOCs help clients find and maintain good jobs, stick to realistic...

The Collaborative to Advance Social Health Integration (CASHI) is composed of a community of 21 innovative primary care teams and community partners committed to increasing the number of patients, families and community members who have access to the essential resources they need to be healthy....

A tax refund is often the largest amount of money a low-income household will receive throughout the year. It offers a unique opportunity to think long term and save for the future. Thus, in 2018, Momentum launched a new pilot program called Tax Time Savings (TTS), presented by ATB. It was through...

In this report, The Common Cents Lab and MetLife Foundation share findings from the experiments we have run over the past several years with VITA providers to improve tax-related outcomes. We encourage you to consider implementing these ideas and engaging in additional conversations about how to...

A lack of emergency savings renders low-income households vulnerable to material hardships resulting from unexpected expenses or loss of income. Having emergency savings helps these households respond to unexpected events, maintain consumption, and avoid high-cost credit products. Because many...

This study uses data from the Longitudinal and International Study of Adults (LISA) to analyze the association between health and household income. Using data on both self-reported general health and self-report mental health, as well as self-reported labour-market outcomes and linked tax records,...

This report is a three-year evaluation of the Financial Empowerment Center initiative’s replication in 5 cities (Denver, CO; Lansing, MI; Nashville, TN; Philadelphia, PA and San Antonio, TX). Financial Empowerment Centers (FECs) offer professional, one-on-one financial counseling as a free...

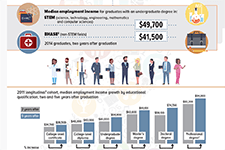

This infographic from Statistics Canada shows the labour market outcomes for college and university graduates between 2010 and 2014. It shows the median employment income achieved by graduates of different education levels, 2 years and 5 years post-graduation. Overall, it shows that people with...

Children’s education savings accounts are a vital tool in boosting high school completion rates, increasing post-secondary education attainment, and reducing poverty. Research shows that saving for a child’s education is connected to improved child development, greater educational and career...

More than half of all employees in the United States report that they are financially stressed, and nearly one in three employees reports being distracted by personal financial issues while at work. This financial stress impacts individuals’ health, relationships, productivity, and time away...

This brief describes the data collected and lessons gleaned from the Financial Coaching Impact & Evaluation Fellowship, which took place over the course of 10 months in 2017. Ultimately, this brief argues that the Financial Well-Being Scale and the Financial Capability Scale are promising...

Building savings is a fundamental strategy for empowering individuals and families with low incomes. Even relatively small amounts of savings can serve as a buffer against inevitable financial shocks that can otherwise undermine social service efforts and successes – and short-term savings offer...

This brief examines the findings of three studies—one from The Pew Charitable Trusts and two commissioned by Pew with support from the W.K. Kellogg Foundation—that looked at the effect of asset limits on family finances and state and program costs and...

In this paper, we report our findings from over a dozen interviews with youth apprenticeship coordinators in Wisconsin and Georgia. Although an integrated financial education component is the exception in youth apprenticeship training, we find broad support from our interviewees for the idea that...

These are the webinar slides from the Center for Financial Security webinar on the role of education in retirement...

We characterize rates of intergenerational income mobility at each college in the United States using administrative data for over 30 million college students from 1999-2013. First, access to colleges varies greatly by parent income. Second, children from low and high-income families have very...

This is a presentation from Behavioural Economics in Action at Rotman, on financial behaviour and financial literacy. It discusses the RESP / Canada Learning Bond enrolment as an applicaiton for behavioural economics research to improve...

These are the webinar slides from the Center for Financial Security webinar on the LIFT-UP program approach to municipal financial empowerment with the National League of...

Comprehensive research on microfinance and subsidy shows that virtually all microfinance institutions are subsidized, but these subsidies are small. There are two clear paths for increasing microcredit’s impact through continued investment: » Lowering the cost of microcredit by lowering...